Development of a testing system for trading algorithms on large arrays of historical market data. The feature was that strategies could have hundreds of thousands of different parameter combinations.

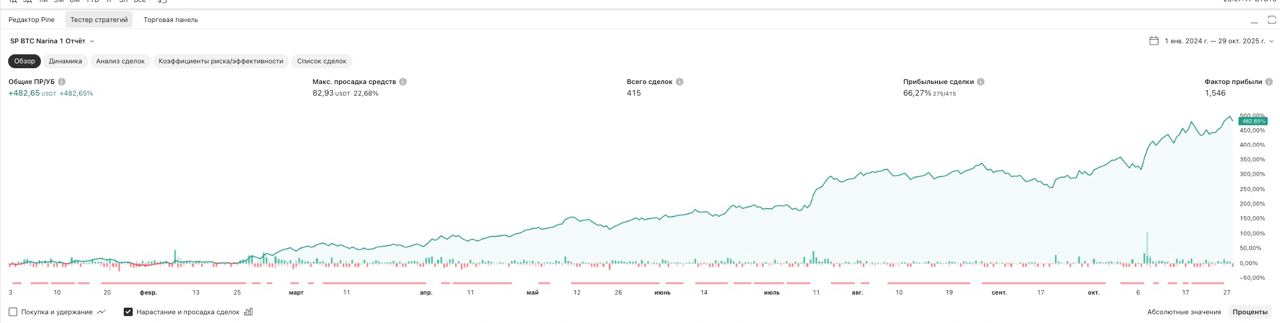

It was possible to implement backtesting of a million parameter combinations over a 2-year history in 2 hours.

Tasks I solved:

Big data processing: Organized work with massive volumes of historical market data.

Mathematical calculations: Implemented complex logic, including matrix calculations and vectorization of operations for maximum processing speed.

Performance optimization: Used the Numba library for JIT compilation and eliminating performance bottlenecks in the system core.

Key skills: Python, Pandas, NumPy, Numba, Data Engineering, Algorithmic Trading, Matrix calculations, Vectorization.

It was possible to implement backtesting of a million parameter combinations over a 2-year history in 2 hours.

Tasks I solved:

Big data processing: Organized work with massive volumes of historical market data.

Mathematical calculations: Implemented complex logic, including matrix calculations and vectorization of operations for maximum processing speed.

Performance optimization: Used the Numba library for JIT compilation and eliminating performance bottlenecks in the system core.

Key skills: Python, Pandas, NumPy, Numba, Data Engineering, Algorithmic Trading, Matrix calculations, Vectorization.